For the past week, we have all been watching the Russian invasion of Ukraine with fear and uncertainty. While our concern lies first and foremost with the lives of innocent Ukrainians, we are also left worrying about how these dramatic events will shape international relations and the global economy — today, and for the long term. Those of us in the supply chain are monitoring the situation closely, scrambling to keep goods moving despite hazardous conditions, border controls, sanctions, and other ever-shifting factors.

Here are the leading indicators we’re watching as the situation continues to unfold:

As we reported last week, an increasing number of Asia-to-Europe shipments are moving to ocean and air freight, rather than rail. Rail routes from Asia to Europe are no longer safe or reliable, as they must pass through Russia before moving to Poland and beyond.

While the most urgent shipments are being moved to the air, the vast majority of goods are being placed onto ships. This is putting even more stress on ocean capacity, which was already being stretched to its limits due to repeated pandemic-related shocks.

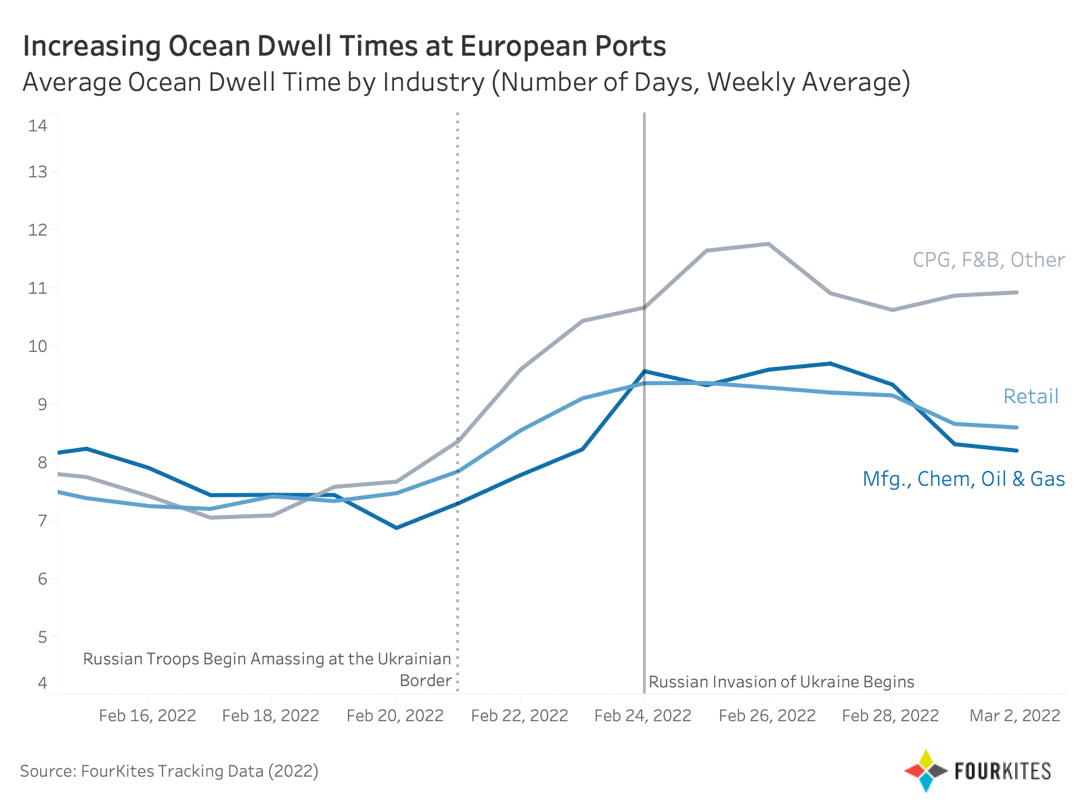

According to the latest data from FourKites’ platform, ocean dwell times have increased in Europe since troops began amassing on the Ukrainian border. As of March 2, export dwell times for all European ports have increased by 25% since February 17. Transshipment dwell times for European ports have increased by 43% over the same period.

![]()

Dwell times have been impacted across Europe, as well, with dwell times up 41% in Western Europe, 6% in Eastern Europe, 26% in Southern Europe, and 17% in Northern Europe between February 17th and March 2nd.

As a result, ocean freight rates are skyrocketing past their already record highs. Our experts anticipate as much as a 20- to 40-fold increase in ocean freight rates. Indeed, this is already happening; where shipments from Shanghai to Rotterdam were less than $2,000 two years ago, some freight forwarders showed rates at $54,000 for a single container immediately after the invasion began. We should expect to see air freight prices increasing in a similar fashion.

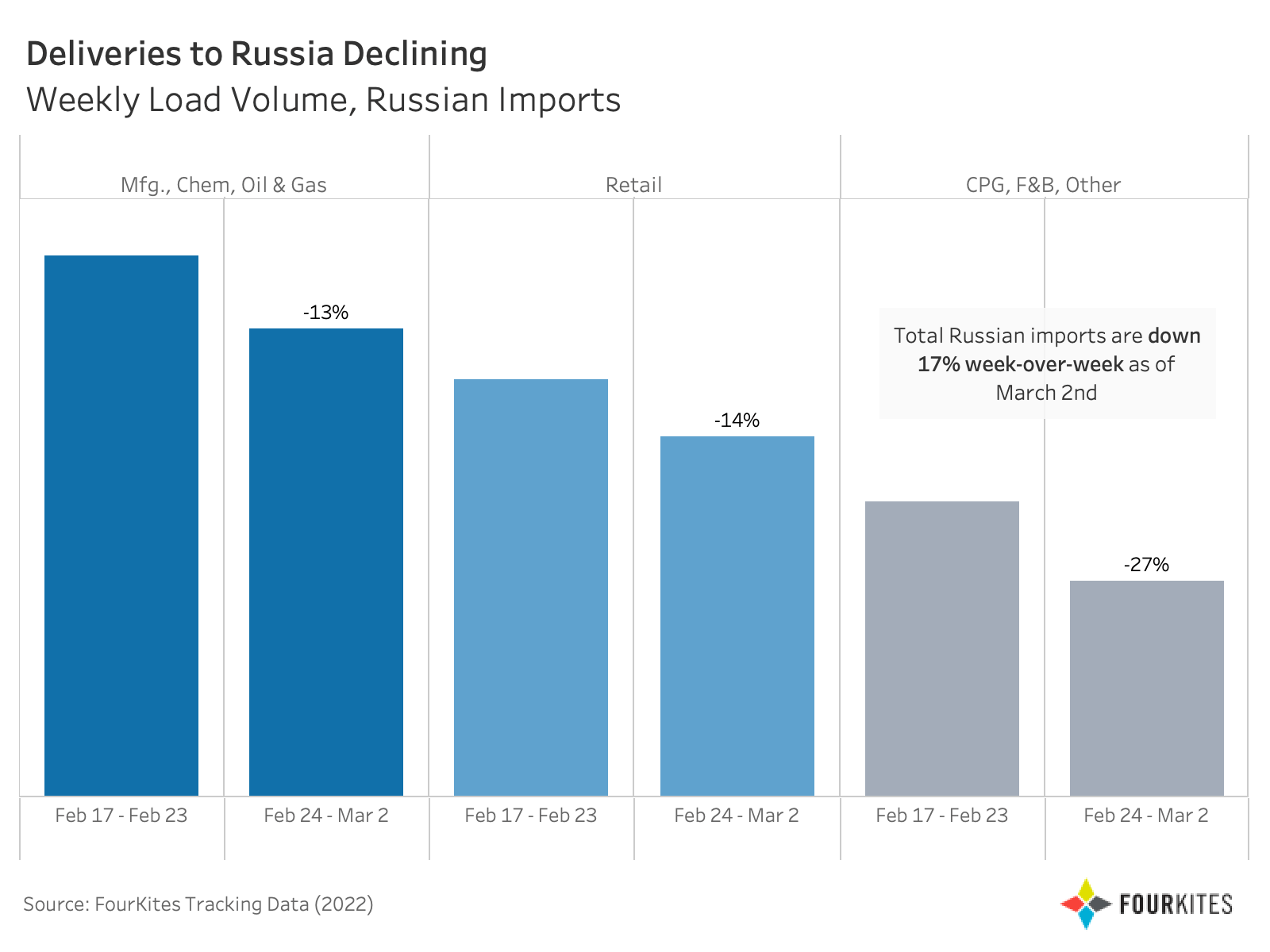

Predictably, the volume of shipments into Russia has plummeted — already down 17% compared to February 17th. This is due to several factors, from sanctions to treacherous routes. Many shippers have pulled out of the region after facing dangerous conditions at the ports, including incidences of friendly fire. And as popular opinion against the violent incursion crystalizes, individual retailers and major brands are also choosing to suspend business with Russia.

What will happen to all those goods? It’s possible that Western companies no longer shipping or selling into Russia will divert their products elsewhere, so shelves will fill up faster in the Americas and other regions. As of today, most of those goods are likely still sitting in Asia, waiting to hitch a ride elsewhere.

While we might see a bump in capacity in Europe – all the trucks and containers that had been headed for Russia will need new destinations, and demand for intra-European road transport could decline – the war is also likely to exacerbate the labor issue, compounding the problems the region is facing.

The conflict is shedding light on how important this region is to global trade. While Ukraine is popularly known as the breadbasket of Europe, we’re facing uncertainty that goes way beyond wheat or vodka.

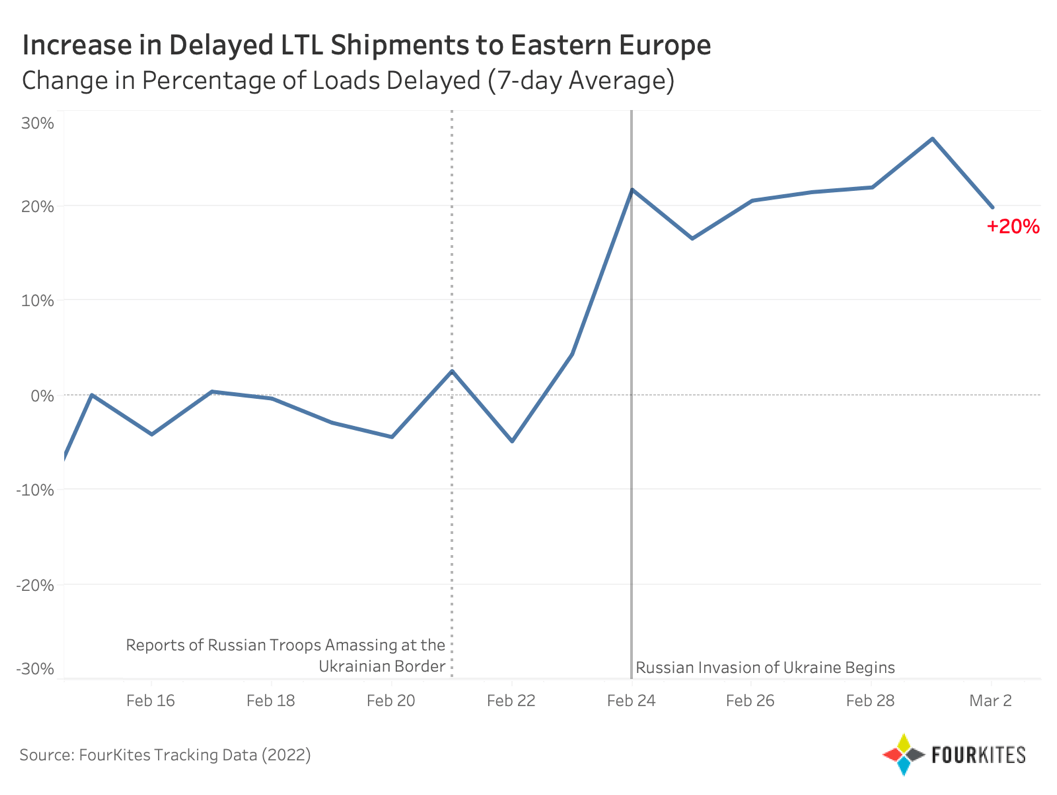

Unsurprisingly, we are seeing an increase in delayed shipments in the region. Among LTL loads traveling into Eastern Europe, the percentage of delayed loads has increased by 20% since before the invasion began.

What types of goods might experience price and supply volatility as a result of the conflict? Oil and gas are dominating the headlines, and we’re already seeing spikes at the pump. And a staggering 25% of the world’s grain — mostly wheat — comes from this region. But we should also keep an eye on the supply of metals found in Ukraine, such as nickel, which is used in batteries. And in worse news for the already strained automobile industry, Ukraine is also rich in palladium, which is used in catalytic converters.

In all these goods and beyond, the longer the conflict drags on, the greater supply shocks we’ll see, resulting in higher consumer prices for everything from bread to batteries to Buicks.

Eclipsing any uncertainty around catalytic converter supply is uncertainty around the severity, length and cost of this conflict — both in terms of economic health and human life. If the conflict reaches a peaceful conclusion soon, we may avoid long-term economic ramifications, especially here in North America. But the longer the conflict continues, the farther its devastation will be felt.

In the meantime, we will continue to monitor the situation closely, and support our customers and communities through end-to-end supply chain visibility to prepare for — and mitigate — whatever might come next.